Starting your own business? Congratulations! But hold on a second, with all the excitement comes that little complicated thing called “Bookkeeping”. In this guide, I want to take you through the fundamentals of small business bookkeeping — from setting up your system to cash flow management, tax preparedness and common mistakes to avoid.

When you finish reading, you will have every bookkeeping tip for small business owners to help create a solid foundation and position yourself for lasting success.

How to manage bookkeeping for small businesses

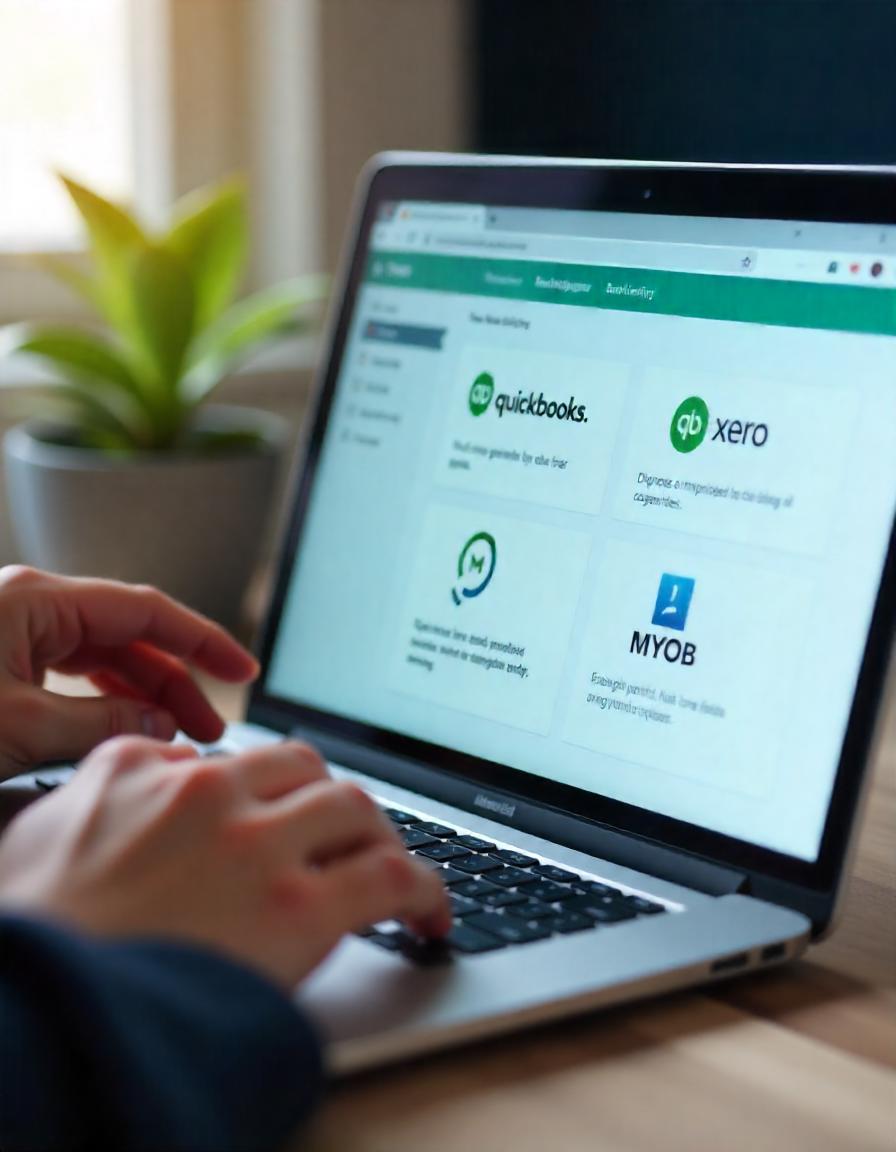

Pick the right software for your requirements; simple bookkeeping tools like QuickBooks, Xero or MYOB can help in streamlining all your bookkeeping activities. It includes functions such as transaction recording, invoicing and expense monitoring. After the setup, create a weekly schedule to sort every expense and income into categories so your records are bright and handy. Once a month you will need to review and reconcile your accounts. And finally, take advantage of the reporting functions in the software to create reports on cash flow, profit, and loss—providing a simple overview of your business finances.

Right now, let us address this step by step for new business owners.

1. Start with a Strong Bookkeeping Foundation

If you are not used to bookkeeping, do not worry, it seems much harder than it actually is, but setting good practice now will really reward you in the future. Essentially bookkeeping is centered on the proper recording of transactions and maintaining record as well. Today, you have two options for bookkeeping, that is single-entry bookkeeping or the more complex double-entry bookkeeping system.

- Using single-entry bookkeeping is rather straightforward it is simply like you were maintaining a chequebook register. If the volume of transactions you are processing is minimal, it is ideal.

- Most small businesses opt for double-entry bookkeeping. Using this method, every transaction is recorded twice; as a debit and credit which provides you with a complete view of your financials.

If you start the right way from the beginning, you will be able to keep clear and true records from day one. Choosing wisely your mortgage broker Melbourne or SMSF services now can help you avoid the time, cost and stress of the wrong landlord down the road.

2. Set Up Your Bookkeeping System with Software

Irrespective of this, you have to have a good bookkeeping method—now this needs a program. Small businesses which are in their early stages of development can find doing bookkeeping using modern tools like QuickBooks or Xero, or MYOB, quite easy.

Why software?

- Automation: Embrace software to do the heavy lifting in all of those repeatable tasks, leaving your day open for scaling your business.

- Fewer Mistakes: Minimizing entry through automation helps eliminate mistakes, producing reliable and constant records.

- Instant Reports: Invest in one Click and get the reports to tell you the exact financial state of your business.

3. Record Every Transaction Daily

This might seem obvious, but is sooo powerful: log every transaction on a daily basis. Every sale, every purchase, every expense — everything counts. Missing a single small transaction can ruin the documents, which will create you problems in future.

- Be Consistent: By recording daily this creates a convention and maintaining your books will be trustworthy/dependable.

- Categorize Properly: Place a transaction in the correct category such as “sales,” “office supplies” and “marketing expenses.” So you can better track your expenses throughout the year and make tax season less painful.

- Organize & keep Receipts: Store each and every Receipt, either electronically or physically. And trust me, you will want them when it comes to reviewing your expenses or preparing taxes.

Keeping your daily records helps you maintain clarity, specificity and structure in small business bookkeeping. And a guide, like this bookkeeping guide for beginners with step-by-step instructions, can save you headaches in the long run.

4. Frequency of performing Account Reconciliation Gratis

Account reconciliation may sound like something very technical, in real essence, it simply involves comparing the records you have with your bank statements and vice versa, to ensure that everything is in order. Account reconciliifications should be done often so that there is early detection of errors and ensure the accounts books are accurate.

So here is what you need to do in order to make a reconciliation of your accounts:

- Compile Records: Obtain your statements and journal records for dates that will be applicable.

- Match Each Entry: Review one line at a time to ensure that each transaction you see on your statement has a corresponding entry in your books.

- Follow-Up On Discrepancies: If anything sticks out, then investigate immediately — this could be an error in recording a transaction or may indicate a missing transaction.

By reconciling accounts on a regular basis, you will not only keep your books correct but also feel sure of your small business bookkeeping.

5. Manage Cash Flow Effectively

Cash flow is to your business as heartbeat is to our body. A steady cash flow will create a buffer against any unexcepted ovned business challenges. Cash flow tracking is not a matter of watching the bonkers out and spending it even — this is a guide you can follow to keep your business alive, whatever happens.

To manage your cash flow:

- Cash Flow Statement — This report shows the inflow and outflow of cash over time which allows you to see your financial rhythm.

- Watch: Monitor cash flow trends for all categories and business units; Identifying trends early on can prepare you for slow seasons, or even growth.

Good cash flow management of small business helps you to plan the future without thinking much, facilitating growth and stability in business. A decent cash flow will ensure that your business has the appropriate fund to expand itself in wise and moderate proportions.

6. Financial Statements

Financial statements are next on the list hence once you are done with recording transactions and tracking your cash flow. Evaluative reports include management reports which give a broad outlook of business with regard to strategic planning.

Let’s break down the three key financial statements every small business owner should know:

- Balance Sheet: Essentially a statement of what your business owns (Assets) and owes (Liabilities) as well as your equity Think of it as a picture of how your business is doing financially at any one time.

- Income Statement — It’s also known as a profit and loss statement, it displays business’s revenue and expenses, as well as total net income or loss for a selected period of time. So you can know what is highly sold and unprofitable, where costs reduce your net revenues.

- Cash Flow – This report indicates the real movement of cash and thus aids in liquidity management. It is crucial if you care about cash flow management for small business owners since it allows you to understand how money sports wear your business.

Knowledge of these accounts will help determine the basics for your small business bookkeeping essentials and financial decisions.

7. Prepare for Tax Season

Tax season is always going to be tough — so before you start dreading it, remember this; with a little bit of organised small business bookkeeping, it actually doesn’t have to suck. For tax time, you will be prepared appropriately with keeping records consistently that keeps your business lined up to avoid late fees or penalties.

Create a Small Business Bookkeeping Checklist for Tax Season Here is a simple bookkeeping checklist for small businesses during tax season:

- Document all receipts and invoices: Ensure you have documentation for your income and expenses handy digitally or physically.

- Be Aware Of Tax Deadlines — Set alerts for critical tax dates to avoid missing a deadline.

- Tax separate: If you are worried about the money required to be paid, set aside funds for it.

Hopefully, these tax preparation for small businesses tips can help give you the peace of mind that everything is in order going into tax season.

8. Avoid Common Bookkeeping Mistakes

Life is too short to make mistakes — Well, we are sure everyone wants to avoid common Bookkeeping Mistake. Avoid These Common Bookkeeping Mistakes Here:

- Combining Personal and Business Debt: Personal and business expenses should not be mixed at any one point in time.

- Not Saving Receipts: Thus receipts play an important role when creating records, for deduction of tax and during audits and therefore one should ensure that he/she gets as many receipts as possible.

- Neglecting to Regularly Update Your Records: Ensure that you keep your records updated most especially when you are trying not to catch up, everything would be missing.

- Expenses being placed in the wrong category: When an expense does not go in the right category, it distorts and will lead to financial statements that depict a different picture from what is happening within your enterprise.

It happens even in cases where everyone involved has good motives. You can keep the records of accounts and transactions in an accurate manner by as to why they occur and how you can get rid of them, if you learn them.

Some Ideas to Ponder Over on Your Bookkeeper Hiring Process

In some cases, as your business continues to expand, you will begin to note that bookkeeping demands a lot of your time. Finally, it makes sense to turn to a specialist because at this stage making a mistake is extremely unbeneficial, not to say fatal. A competent bookkeeper will also assist in organizing the bookkeeping structure, and preparing taxes as well as planning cash flow management for small businesses.

Benefits of a Professional Bookkeeper:

- Saves You Time: A bookkeeper performs many tasks which can be very time consuming allowing the business person to attend to other more pressing issues in the business.

- Ensures Accuracy: Small business bookkeeping services involve people familiar with various nuances that may lead to mistakes in the proprietor’s hands.

- Provides Strategic Insight: A skilled bookkeeper will be of immense help and will give advice on this matter based on the results obtained from financial records.

When hiring, ensure that the person you hire is conversant with bookkeeping software for small businesses and the industry. So, when you hire the right bookkeeper, then you will be rest assured knowing your finances are in the right hand.

Conclusion

So, I think you are ready to steer the ship of your business to the right financial direction and further develop your bookkeeping knowledge with the help of this guide! These are not just to-do lists; these are the most fundamental elements of the process leading to your success. Managing your books yourself or hiring an expert will only help your business grow and be ready for what’s ahead.

Always consider this, bookkeeping for small businesses is centered not primarily on recording transactions but on providing predictable, making wise and preparing for further advancement. But, learn these small business bookkeeping essentials today and be ready to conquer the business world tomorrow with pride.